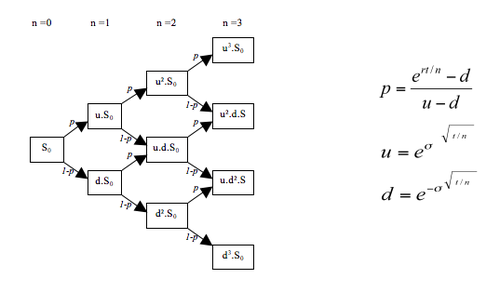

The Binomial options pricing model is a prevalent Lattice model for the valuation of derivatives whose determination of the theoretical options price is predicated on the assumption of two potential prices; hence, the binomial characterization of this model. The two potential options prices vacillate between higher and lower points defining a range. This confers great variability and ambiguity which is subsequently manipulated and constrained by input factors, such as the present asset price, strike price, time until expiry, volatility, risk free rate, and dividend yield of the underlying. The nodes or prices of the option at specific periods of time is measured in relation to these variables and used in the calculation of the options price. A multi period or multi node perspective displays an iterative visualization of changes in the options price according to alterations in any of the preceding conditions. Consequently, the Binomial model grants traders and investors greater insight regarding the optimal date of execution as predicted by the binomial tree which they consult and analyze to ascertain said date. The following links are to an explanatory video by BionicTurtle whose spreadsheets warrant their praise and commendation by many options traders for their utility in the pricing of derivatives, and his Binomial Options Pricing Spreadsheet: https://www.youtube.com/watch?v=lzMQ3hZqtp0, https://www.dropbox.com/s/7e9cacu4b5rpmnr/010119-binomial-2step.xlsx?dl=0

-

The United States' solution to essentially every recession within the past few decades was and is presently to create new currency and r...

-

The Boston-based hedge fund Baupost Group's 3rd Quarter 13F Filing which was released just weeks ago disclosed a 4.3 % portfolio weighti...

-

Bill Ackman in his firm, Pershing Square's recent interim financial statement release to investors makes a rather unconventi...

No comments:

Post a Comment