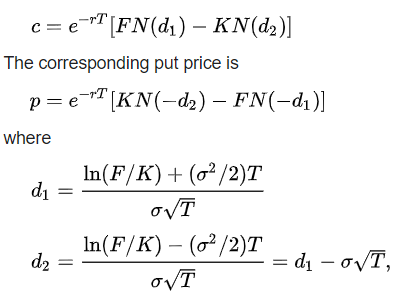

The Black 76 Model developed by Fischer Black of Black-Scholes was first proposed by him in Journal of The American Finance Association in 1976 publishing known as Taxes and The Pricing of Options. In it, he expounds upon various improvements and adaptations of the original Black Scholes model conferring greater versatility for the pricing of other derivatives, such as interest swaps, floors, caps, futures, and limited variable rate securities.

where R = the constant risk free rate ,F(t) is the futures price of a particular underlying with that is log-normal with constant volatility σ. The Black 76 Model states the price of European call option at maturity T corresponding to a future conferring a strike price K and delivery date.

Criticism

No comments:

Post a Comment