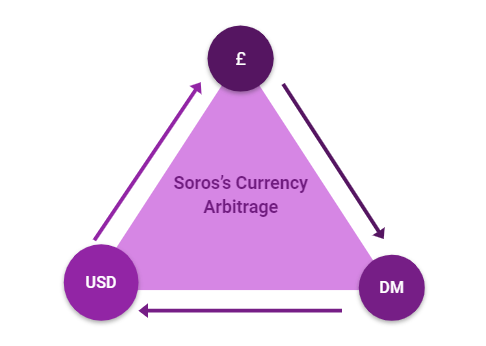

Triangular currency arbitrage is the successive exchange of three currencies when a discrepancy exists among them in a specific consecutive order by which sequential transactions and conversions occur facilitated in modernity by an automated computerized algorithm that detects for these arbitrage opportunities and exploits them with expedience and precision. A alternative example of triangular currency arbitrage is George Soro’s exploitation of Britain’s ERM (Exchange Rate Mechanism on September 16, 1992 infamously known as Black Wednesday. Soros noticed that the ERM enforced a fixed 2.7 Mark / Pound exchange rate despite the Pounds gross inflation which was fundamentally unstable and began borrowing pounds from banks. He then sold his Pounds for Marks that he continually held while repeating this process as it gained momentum at other funds and brokerage houses. Subsequently, the value of the pound plummeted against that of the Mark, and Soros bought back his originally borrowed Pounds at a fraction of the cost retaining a $1Bln profit or $15.00 for every British citizen in 1992 as estimated by the Wall Street Journal.

Triangular currency arbitrage is the successive exchange of three currencies when a discrepancy exists among them in a specific consecutive order by which sequential transactions and conversions occur facilitated in modernity by an automated computerized algorithm that detects for these arbitrage opportunities and exploits them with expedience and precision. A alternative example of triangular currency arbitrage is George Soro’s exploitation of Britain’s ERM (Exchange Rate Mechanism on September 16, 1992 infamously known as Black Wednesday. Soros noticed that the ERM enforced a fixed 2.7 Mark / Pound exchange rate despite the Pounds gross inflation which was fundamentally unstable and began borrowing pounds from banks. He then sold his Pounds for Marks that he continually held while repeating this process as it gained momentum at other funds and brokerage houses. Subsequently, the value of the pound plummeted against that of the Mark, and Soros bought back his originally borrowed Pounds at a fraction of the cost retaining a $1Bln profit or $15.00 for every British citizen in 1992 as estimated by the Wall Street Journal.Triangular Currency Arbitrage

Triangular currency arbitrage is the successive exchange of three currencies when a discrepancy exists among them in a specific consecutive order by which sequential transactions and conversions occur facilitated in modernity by an automated computerized algorithm that detects for these arbitrage opportunities and exploits them with expedience and precision. A alternative example of triangular currency arbitrage is George Soro’s exploitation of Britain’s ERM (Exchange Rate Mechanism on September 16, 1992 infamously known as Black Wednesday. Soros noticed that the ERM enforced a fixed 2.7 Mark / Pound exchange rate despite the Pounds gross inflation which was fundamentally unstable and began borrowing pounds from banks. He then sold his Pounds for Marks that he continually held while repeating this process as it gained momentum at other funds and brokerage houses. Subsequently, the value of the pound plummeted against that of the Mark, and Soros bought back his originally borrowed Pounds at a fraction of the cost retaining a $1Bln profit or $15.00 for every British citizen in 1992 as estimated by the Wall Street Journal.

Subscribe to:

Posts (Atom)

-

The United States' solution to essentially every recession within the past few decades was and is presently to create new currency and r...

-

The Boston-based hedge fund Baupost Group's 3rd Quarter 13F Filing which was released just weeks ago disclosed a 4.3 % portfolio weighti...

-

Bill Ackman in his firm, Pershing Square's recent interim financial statement release to investors makes a rather unconventi...

No comments:

Post a Comment